Last week, LM Funding America, Inc. (LMFA) came onto our radar screen as a heavy volume, small-float stock with potential for a big move like Yulong Eco-Materials Limited (YECO). We provided an updated report on Tuesday. Yesterday LMFA traded heavily, with over 6 million shares traded and was up over 30% but got slammed back down to $1.57 on light volume at the end of the day. While it is frustrating, we think that is a positive sign as it is very closely mirroring what YECO did before its massive 1000% run in two days in October. We are up to 731 followers despite not giving out a lot of alerts, a fact that we think is indicative of a successful, diligent and prudent stock picking history. If you like our picks you can follow our blog by clicking the follow button on the top of the left hand panel. You can also follow us on Twitter @StockTradePicks. We have over 3,300 followers on Twitter as well.

Let's have a look at yesterday's chart:

We can see that most of the volume were buys (green bars) and that the heaviest trading took place above $1.90 to the day high of $2.18 at around 2pm. Comparatively light volume at 2:45 and 3:30 caused it to crash back down. What does this mean? It's obvious that shorters and market makers were fishing for stop losses and it worked. The exact same thing happened on November 14. LMFA has a ridiculously small float (about 400,000 or 1,100,000 depending on which source of information you use) so it is easy to control the stock price, frustrating day traders and getting them to trigger stop losses or otherwise have them sell at a loss. This is the easy way to pick up cheap shares and we believe that is what is happening here. Given the high volume compared to the float, the only conclusion can be this is either from dilution or shorting. One would fear dilution but we strongly disagree with that and if you read further on in the report you'll understand why. Financing recently took place at $2.40 and those shares are with long-term holders.

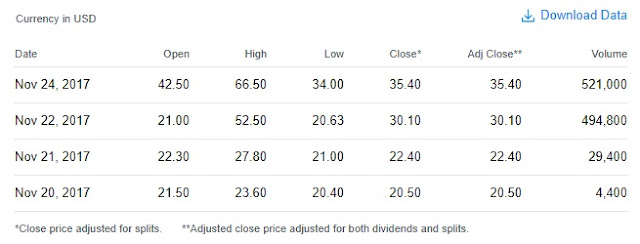

For those who are stuck in LMFA at a loss, we will tell them not to be discouraged. LMFA has a history of performing a Thanksgiving special. Look what happened last year on the day before and the day after Thanksgiving:

This is adjusted for a 1-for-10 split. On the Wednesday before Thanksgiving, LMFA started at $2.10, shot up to $5.25 but was pushed down back to $3.01 by the end of the day, leaving a lot of frustrated traders. However, the Friday after Thanksgiving it shot up to $6.65 before closing at $3.54. So for those who want a second chance to play LMFA for profits, history has suggested that Friday will be good for that. $2.40 would be a good minimum target and we will explain why. We think this has potential to be a YECO-type mover, but if people want to play for lesser, more short-term profits, they can do that as well. Someone with the ability to do so is obviously shorting this stock, for whatever reason. If they take a day off tomorrow and won't be there to frustrate day traders and momentum players, a short squeeze could take place. Fintel shows that of the 6 million shares traded yesterday, 1.5 million was short. Following up on last Wednesday's performance where 1.4 million of 6.5 million shares were short. Given the small float, this is highly likely naked short selling, unless shorts are shorting and covering several times a day. .

A few weeks ago, LMFA dropped after a reverse split and financing deal that doesn't make much sense. The company received $6 million, way more cash than it needs. After doing substantial research into the background of the major buyer, we believe that this transaction will be a prelude to a larger one - either a buyout, a reverse takeover or some other kind of corporate transaction - that could result in a substantial price rise similar to what happened to YECO. Why do we think LMFA can run like YECO? The businesses are very different but the stories, news flow and price action are quite similar.

On August 22, YECO first announced the agreement to acquire the Millennium Sapphire. The purchase price was for $50 million with 25 million shares to be issued at $2.00. The stock price initially reacted very positively, going as high as $2.71, but by the end of the day it was down to $2.07 and back to where it started within a few days.

This transaction that took place at $2.00 for 25 million shares, or more than 10 times the float at the time, caused the stock price to rise over 1000% from $1.52 to $17.87 in two days. The stock is still over $6.00, three times higher that the price of the transaction. The move wasn't even based on new news, but the closure of the transaction that was already known by the market for two months. Certainly if there was excitement over acquiring the Millennium Sapphire, investors could have bought it in August or September, right? Retail traders were mainly following the price action set up by the market makers so that they would sell to them cheaply because they didn't understand the value of this deal.

Why is this similar to LMFA? LMFA closed a financing transaction at $2.40. When this 13D filing was disclosed on November 14, the following price action happened:

Huge volume and a temporary price spike on November 14 gave way and the stock is now lower than ever. This may be seen as a bad sign by traders, but it is in fact a GOOD sign. Just like YECO, the market makers and shorts sucked in a bunch of day traders on the day of the news and are forcing them to give up and sell back shares cheaply because they think the stock is dead. Just like YECO, LMFA is not at all dead. We believe that some kind of transaction will take place along the lines of YECO - either a buyout, reverse takeover or other type of major corporate transaction - that can result in a similar type of run based on what we have just seen. The people who bought large into the $2.40 financing deal did not do so to lose money. They are experienced market players.

Before getting into the deal, we will talk briefly about what LMFA does, because once you understand that, the rest of the pieces will make sense. LMFA is basically a bad debt buyer that tries to collect on overdue bills from problem tenants. From LMFA's website:

"Formed in January 2008, LM Funding is a financial services company that purchases delinquent accounts from community associations. We offer community associations a variety of financial products customized to an association’s financial needs.

We believe that condo associations and their owners shouldn’t have to take on the financial responsibility of delinquency and the hassle of collection. That’s why we “buy problems.” Before LM Funding, condo association owners would have to hire attorneys to collect bad debt. We’re changing that, with a unique business idea that turns debt into instant cash—freeing condo associations from the burden of collection and allowing them to continue to maintain their operations. LM Funding’s accumulated delinquent assessment balance is now in excess of $150 million. That is a lot of problems that we’ve bought, and we want more!"

This business plan has obviously not been that great if you look at the stock price and history of operating losses, save for a few quarters. LMFA plummeted in price after a 1-for-10 reverse split and the financing at $2.40, which at that time was below the market price. From the Q3 press release:

"On November 1, 2018, the Company closed an underwritten public offering that included the underwriters’ exercise of its option to purchase additional shares, which resulted in the issuance of 2,875,000 shares of its common stock (or pre-funded warrants to purchase common stock in lieu thereof) and common warrants to up to 2,875,000 shares of the Company’s common stock. At closing, LM Funding received gross proceeds from the offering of approximately $6.0 million, before deducting underwriting discounts and commissions and other expenses payable by the Company. As a result of the offering, the Company’s stockholders’ equity will exceed $2.5 million and its publicly held shares (i.e., shares not held directly or indirectly by an officer, director, or greater-than-10% of the total shares outstanding) will be approximately 1.1 million shares."

So the important thing to extract from this paragraph:

1. The company closed an equity financing of 2.9 million shares at $2.40, bringing in $6 million.

2. The reverse split and cash injection kept the company eligible for listing on the NASDAQ.

3. The float is 1.1 million shares, leaving a lot of possibility for volatility, as witnessed over this past week.

Two more paragraphs to note from the release:

“In the third quarter, we took critical steps to improve our capitalization structure and balance sheet,” said Bruce Rodgers, LM Funding’s Chief Executive Officer. “We were successful in closing a $6 million financing transaction that has significantly improved our financial flexibility and allowed us to regain compliance with NASDAQ. With this additional working capital, we can focus on providing solutions to condominium and homeowner associations.”

"At September 30, 2018, the Company had cash and cash equivalents of $929,149, compared with $590,394 at December 31, 2017. For the nine months ended September 30, 2018, the net cash from our operating and investing activities was a net use of cash of $13,055 as compared to a net use of cash of $1,090,990 for the comparable 2017 period"

The company had over $900,000 in cash as of September 30, 2018 and only spent $13,000 in cash between operating and investing activities for the first nine months of the year. The company didn't need to dilute so much and bring in that much cash. It was probably fine with something like $2 million to remain listed on the NASDAQ. Instead it went for $6 million. This deal does not make any sense - especially since the stock price has tanked to the $1.50's since then - unless there is something more to be disclosed. We believe that there is something going on behind the scenes that investors are unaware of and once that comes to light, LMFA will be a runner.

The clue to look at is in the 13D filing:

All this information is important in figuring out what is truly going on here. Mark Pajak. Craven House Capital. The address and phone number: 107 West Federal St, PO Box 480 Middleburg VA; +1 540 687 3166. There was a Florida address in another part of the 13D filing but that one looks like it belongs to the purchaser's lawyer.

Craven Capital purchased 640,000 units at $2.40 for a 31.45% stake in LMFA. That's a $1,536,000 investment, one of which Craven is already down over $500,000 two weeks after closing the deal.

What's more Craven Capital is a merchant bank that is listed on the LSE and has a market cap of only 6.3 million pounds, about $8 million. Craven released a news release about its purchase of LMFA shares, so it is obviously proud of this major investment:

Craven considers itself to be long-term, patient capital and is involved in "special situations", restructuring, expansion and turn around investments. We can reasonably expect that this is what they will be with LMFA. Craven was allowed to purchase a substantial stake in LMFA, so whatever Craven management has on their minds must have support of LMFA management. In turn, LMFA made the following investment into a Craven holding:

"On November 2, 2018, the Company invested part of the proceeds by purchasing a Securities Purchase Agreement (the “IIU SPA”) from IIU Inc. (“IIU”), a possible synergistic Virginia based travel insurance brokerage company controlled by Craven House N.A. (which owns approximately 27% of the Company’s outstanding stock as of November 13, 2018), pursuant to which IIU issued to the Company a Senior Convertible Promissory Note (“IIU Note”) in the original principal amount of $1,500,000 in exchange for a purchase price of $1,500,000. The maturity date of the Note is 360 dates after the date of issuance (subject to acceleration upon an event of default). The Note carries a 3.0% interest rate, with accrued but unpaid interest being payable on the Note’s maturity date."

The first thing we would like to point out is that LMFA claims that Craven owns 27% of LMFA as of November 13. But the 13D filing and Craven's press release which both came after November 13 claims that Craven owns 31.5% of LMFA. So did Craven buy more LMFA on the open market? Or is this merely an administration error? What we do know is that someone was dumping shares and shorting last Wednesday, but it certainly wasn't Craven given this level of engagement. So one has to wonder why would Craven spend $1.5 million to own over 30% of LMFA when Craven itself is only an $8 million market cap company? LMFA now owns $1.5 million worth of a debt instrument on Craven House's IIU, but the stock given to Craven in return is now worth only around a million dollars. This is a very substantial and important investment to them, not the same as if Citibank were to throw $1.5 million at it, for instance. Craven is in LMFA to enact a substantial transaction, it says so right in its mission statement seen above.

This is not the first time Craven has done something like this. Despite its small size, it has made four acquisitions recently, excluding the stake in LMFA:

Here is a press release about the land acquisition in Brazil:

"The Company today announces that it has acquired the entire share capital of Universal Properties Brasil Administracao de Imoveis Ltda ("UPBAI") for a total cash consideration of USD $3,100,000.

UPBAI is a holding company and as such has no trading activity. Its sole asset is a 500 hectare parcel of land in Canavieiras in the Bahia region of Brazil. The property comprises of four neighboring land parcels and benefits from 7.5km of direct ocean-front real estate.

Mark Pajak, Director, commented:

"We are delighted to announce the acquisition of this outstanding asset which represents our second substantial land holding in Bahia, just a few hundred kilometers from the 1,967 hectare property in Caravelas in which the Company is a minority shareholder. The land owned by UPBAI is ideal for both agricultural use or property development and we look forward to announcing further plans for these properties in due course. We continue to evaluate further land acquisitions in the region.""

It is interesting to see that Craven is into international beach front property development. It sounds kind of like the type of properties that LMFA offers financial solutions for.

So who is Mark Pajak? It is best to ask the man himself, up on the management section of Craven's website:

"Mark Pajak's duties include chairing the investment committee and direct board level involvement with the portfolio companies. Prior to his role at Craven House Capital, Mr. Pajak was Managing Director at Desmond Holdings and a member of their investment committee. He is also President and CEO of DLC Holdings Corp. (formerly Desmond Investments Ltd), a company listed on the TSX Venture Exchange in Toronto.

Mr. Pajak started his career at Taylor Wimpey Plc, the UK's largest property developer where he worked directly for the Chief Executive advising on M&A activity, corporate capital structuring and communications with shareholders and the financial community. He was among the youngest directors in the 130 year history of the company.

Mark holds both an undergraduate degree and MBA from Oxford University."

Note the two highlighted pieces. Mr. Pajak is the CEO of DLC on the Toronto Stock Exchange and worked with a property developer, specifically advising in M&A activities. Let's check out what DLC is up to:

DLC is a shell that will have a reverse takeover to publicly list Craven, and Ceniako, one of Craven's four acquisitions listed above. KwikBuild, noted as a company related to Craven, is a South African builder of homes.

So now we know that the head of the firm that purchased more than 30% of LMFA's shares has bought private companies and then taken them public through reverse takeovers in the past. Companies with beach front properties. In our opinion at a minimum, Mr. Pajak would be purchasing LMFA shares to expand its financing business to some of his other deals.

Recall the final piece of this puzzle. The address and phone number used by Mark Pajak on the 13D filing:

107 West Federal St, PO Box 480 Middleburg VA

+1 540 687 3166

Here it is again, owned by Wallach & Company:

While small companies do often share office space, it would be unusual to see them share a PO Box number and phone number. What's more, Wallach is the only company associated with this address other than Craven when doing an internet search. Wallach doesn't seem too active, for instance, there are no Yelp or BBB reviews. But there is one news article about this insurance company and it serves 15,000 clients a year. So it is a small operation that seems to focus on health insurance to those who are travelling abroad. This is very likely the synergistic Virginia based travel insurance brokerage company that LMFA made mention of in its Q3 results.

So what does all this stuff mean?

Craven House Capital made a significant investment - both in terms of a large stake and a high proportion of its funds - into LMFA. LMFA provides financial solutions for condo associations. Craven has a history of doing reverse takeover transactions and invests in property development projects. What's more, it shares a mailing address and phone number of a company that offers health insurance to those travelling abroad and used that specific address on its 13D filing with the SEC.

What is our conclusion from all this? Craven's investment into LMFA is part of something bigger. We strongly believe that there will be a reverse takeover, just like with DLC in Canada, and it could involve one or more of Craven's other assets. Development of a resort property in Brazil might be where this is headed.

If you were caught at a bad price in the volatile trading of LFMA recently, do not fear. Craven House Capital likely has big plans for this investment. Look at what happened to YECO when it announced the close of its reverse merger deal to buy the Millennium Sapphire.

Disclosure: We are long LMFA

Bitcoin has gone from a concept worth pennies a few years ago to worth thousands of dollars. It may appear to some who are late to the game that the opportunity to get rich is gone. However, there are still plenty of ways to make some money trading in bitcoin and other cryptocurrency. Here are some links to valuable reports and strategies:

The Cryptocurrency Codex from the Cryptocurrency Institute

Secrets To Unlimited Free Bitcoin

The Crypto-Currency Evolution eBook

Bitcoin Complete Guide for Dummies

The Bitcoin Miracle Guide

The Bitcoin Cheat Code Book

The Crpytocurrency Course

Bitcoin Investing Live

If you're interested in making money investing or trading the stock market, here are some good resources to assist you. This includes technical analysis, investing in the weed sector, dividend stock investing, gold and commodities, sector rotation, options trading and microcap trading strategies.

Microcap Millionaires Free Video: Cheap Gold Miner Set to Soar in Fall 2017

The dividend stock report from dividendstocksonline.com

Let's have a look at yesterday's chart:

We can see that most of the volume were buys (green bars) and that the heaviest trading took place above $1.90 to the day high of $2.18 at around 2pm. Comparatively light volume at 2:45 and 3:30 caused it to crash back down. What does this mean? It's obvious that shorters and market makers were fishing for stop losses and it worked. The exact same thing happened on November 14. LMFA has a ridiculously small float (about 400,000 or 1,100,000 depending on which source of information you use) so it is easy to control the stock price, frustrating day traders and getting them to trigger stop losses or otherwise have them sell at a loss. This is the easy way to pick up cheap shares and we believe that is what is happening here. Given the high volume compared to the float, the only conclusion can be this is either from dilution or shorting. One would fear dilution but we strongly disagree with that and if you read further on in the report you'll understand why. Financing recently took place at $2.40 and those shares are with long-term holders.

For those who are stuck in LMFA at a loss, we will tell them not to be discouraged. LMFA has a history of performing a Thanksgiving special. Look what happened last year on the day before and the day after Thanksgiving:

This is adjusted for a 1-for-10 split. On the Wednesday before Thanksgiving, LMFA started at $2.10, shot up to $5.25 but was pushed down back to $3.01 by the end of the day, leaving a lot of frustrated traders. However, the Friday after Thanksgiving it shot up to $6.65 before closing at $3.54. So for those who want a second chance to play LMFA for profits, history has suggested that Friday will be good for that. $2.40 would be a good minimum target and we will explain why. We think this has potential to be a YECO-type mover, but if people want to play for lesser, more short-term profits, they can do that as well. Someone with the ability to do so is obviously shorting this stock, for whatever reason. If they take a day off tomorrow and won't be there to frustrate day traders and momentum players, a short squeeze could take place. Fintel shows that of the 6 million shares traded yesterday, 1.5 million was short. Following up on last Wednesday's performance where 1.4 million of 6.5 million shares were short. Given the small float, this is highly likely naked short selling, unless shorts are shorting and covering several times a day. .

A few weeks ago, LMFA dropped after a reverse split and financing deal that doesn't make much sense. The company received $6 million, way more cash than it needs. After doing substantial research into the background of the major buyer, we believe that this transaction will be a prelude to a larger one - either a buyout, a reverse takeover or some other kind of corporate transaction - that could result in a substantial price rise similar to what happened to YECO. Why do we think LMFA can run like YECO? The businesses are very different but the stories, news flow and price action are quite similar.

On August 22, YECO first announced the agreement to acquire the Millennium Sapphire. The purchase price was for $50 million with 25 million shares to be issued at $2.00. The stock price initially reacted very positively, going as high as $2.71, but by the end of the day it was down to $2.07 and back to where it started within a few days.

The market makers had frustrated day traders and they were back to selling shares at a loss, well below the agreed to price of $2.00. Once the day traders were flushed out and shares were accumulated cheaply by others, look what happened once the transaction closed on October 17:

Why is this similar to LMFA? LMFA closed a financing transaction at $2.40. When this 13D filing was disclosed on November 14, the following price action happened:

Huge volume and a temporary price spike on November 14 gave way and the stock is now lower than ever. This may be seen as a bad sign by traders, but it is in fact a GOOD sign. Just like YECO, the market makers and shorts sucked in a bunch of day traders on the day of the news and are forcing them to give up and sell back shares cheaply because they think the stock is dead. Just like YECO, LMFA is not at all dead. We believe that some kind of transaction will take place along the lines of YECO - either a buyout, reverse takeover or other type of major corporate transaction - that can result in a similar type of run based on what we have just seen. The people who bought large into the $2.40 financing deal did not do so to lose money. They are experienced market players.

Before getting into the deal, we will talk briefly about what LMFA does, because once you understand that, the rest of the pieces will make sense. LMFA is basically a bad debt buyer that tries to collect on overdue bills from problem tenants. From LMFA's website:

"Formed in January 2008, LM Funding is a financial services company that purchases delinquent accounts from community associations. We offer community associations a variety of financial products customized to an association’s financial needs.

We believe that condo associations and their owners shouldn’t have to take on the financial responsibility of delinquency and the hassle of collection. That’s why we “buy problems.” Before LM Funding, condo association owners would have to hire attorneys to collect bad debt. We’re changing that, with a unique business idea that turns debt into instant cash—freeing condo associations from the burden of collection and allowing them to continue to maintain their operations. LM Funding’s accumulated delinquent assessment balance is now in excess of $150 million. That is a lot of problems that we’ve bought, and we want more!"

"On November 1, 2018, the Company closed an underwritten public offering that included the underwriters’ exercise of its option to purchase additional shares, which resulted in the issuance of 2,875,000 shares of its common stock (or pre-funded warrants to purchase common stock in lieu thereof) and common warrants to up to 2,875,000 shares of the Company’s common stock. At closing, LM Funding received gross proceeds from the offering of approximately $6.0 million, before deducting underwriting discounts and commissions and other expenses payable by the Company. As a result of the offering, the Company’s stockholders’ equity will exceed $2.5 million and its publicly held shares (i.e., shares not held directly or indirectly by an officer, director, or greater-than-10% of the total shares outstanding) will be approximately 1.1 million shares."

So the important thing to extract from this paragraph:

1. The company closed an equity financing of 2.9 million shares at $2.40, bringing in $6 million.

2. The reverse split and cash injection kept the company eligible for listing on the NASDAQ.

3. The float is 1.1 million shares, leaving a lot of possibility for volatility, as witnessed over this past week.

Two more paragraphs to note from the release:

“In the third quarter, we took critical steps to improve our capitalization structure and balance sheet,” said Bruce Rodgers, LM Funding’s Chief Executive Officer. “We were successful in closing a $6 million financing transaction that has significantly improved our financial flexibility and allowed us to regain compliance with NASDAQ. With this additional working capital, we can focus on providing solutions to condominium and homeowner associations.”

"At September 30, 2018, the Company had cash and cash equivalents of $929,149, compared with $590,394 at December 31, 2017. For the nine months ended September 30, 2018, the net cash from our operating and investing activities was a net use of cash of $13,055 as compared to a net use of cash of $1,090,990 for the comparable 2017 period"

The company had over $900,000 in cash as of September 30, 2018 and only spent $13,000 in cash between operating and investing activities for the first nine months of the year. The company didn't need to dilute so much and bring in that much cash. It was probably fine with something like $2 million to remain listed on the NASDAQ. Instead it went for $6 million. This deal does not make any sense - especially since the stock price has tanked to the $1.50's since then - unless there is something more to be disclosed. We believe that there is something going on behind the scenes that investors are unaware of and once that comes to light, LMFA will be a runner.

The clue to look at is in the 13D filing:

All this information is important in figuring out what is truly going on here. Mark Pajak. Craven House Capital. The address and phone number: 107 West Federal St, PO Box 480 Middleburg VA; +1 540 687 3166. There was a Florida address in another part of the 13D filing but that one looks like it belongs to the purchaser's lawyer.

Craven Capital purchased 640,000 units at $2.40 for a 31.45% stake in LMFA. That's a $1,536,000 investment, one of which Craven is already down over $500,000 two weeks after closing the deal.

What's more Craven Capital is a merchant bank that is listed on the LSE and has a market cap of only 6.3 million pounds, about $8 million. Craven released a news release about its purchase of LMFA shares, so it is obviously proud of this major investment:

Look at the bottom of the news release, about Craven:

"The Company's Investing Policy is to invest in or acquire a portfolio of companies, partnerships, joint ventures, businesses or other assets globally in any geographic jurisdiction. The company will invest in both developed and developing markets providing long term patient capital and is often involved in special situations, restructuring, expansion and turn around investments in crisis and transitioning economies."

Craven considers itself to be long-term, patient capital and is involved in "special situations", restructuring, expansion and turn around investments. We can reasonably expect that this is what they will be with LMFA. Craven was allowed to purchase a substantial stake in LMFA, so whatever Craven management has on their minds must have support of LMFA management. In turn, LMFA made the following investment into a Craven holding:

"On November 2, 2018, the Company invested part of the proceeds by purchasing a Securities Purchase Agreement (the “IIU SPA”) from IIU Inc. (“IIU”), a possible synergistic Virginia based travel insurance brokerage company controlled by Craven House N.A. (which owns approximately 27% of the Company’s outstanding stock as of November 13, 2018), pursuant to which IIU issued to the Company a Senior Convertible Promissory Note (“IIU Note”) in the original principal amount of $1,500,000 in exchange for a purchase price of $1,500,000. The maturity date of the Note is 360 dates after the date of issuance (subject to acceleration upon an event of default). The Note carries a 3.0% interest rate, with accrued but unpaid interest being payable on the Note’s maturity date."

The first thing we would like to point out is that LMFA claims that Craven owns 27% of LMFA as of November 13. But the 13D filing and Craven's press release which both came after November 13 claims that Craven owns 31.5% of LMFA. So did Craven buy more LMFA on the open market? Or is this merely an administration error? What we do know is that someone was dumping shares and shorting last Wednesday, but it certainly wasn't Craven given this level of engagement. So one has to wonder why would Craven spend $1.5 million to own over 30% of LMFA when Craven itself is only an $8 million market cap company? LMFA now owns $1.5 million worth of a debt instrument on Craven House's IIU, but the stock given to Craven in return is now worth only around a million dollars. This is a very substantial and important investment to them, not the same as if Citibank were to throw $1.5 million at it, for instance. Craven is in LMFA to enact a substantial transaction, it says so right in its mission statement seen above.

This is not the first time Craven has done something like this. Despite its small size, it has made four acquisitions recently, excluding the stake in LMFA:

Here is a press release about the land acquisition in Brazil:

"The Company today announces that it has acquired the entire share capital of Universal Properties Brasil Administracao de Imoveis Ltda ("UPBAI") for a total cash consideration of USD $3,100,000.

UPBAI is a holding company and as such has no trading activity. Its sole asset is a 500 hectare parcel of land in Canavieiras in the Bahia region of Brazil. The property comprises of four neighboring land parcels and benefits from 7.5km of direct ocean-front real estate.

Mark Pajak, Director, commented:

"We are delighted to announce the acquisition of this outstanding asset which represents our second substantial land holding in Bahia, just a few hundred kilometers from the 1,967 hectare property in Caravelas in which the Company is a minority shareholder. The land owned by UPBAI is ideal for both agricultural use or property development and we look forward to announcing further plans for these properties in due course. We continue to evaluate further land acquisitions in the region.""

It is interesting to see that Craven is into international beach front property development. It sounds kind of like the type of properties that LMFA offers financial solutions for.

So who is Mark Pajak? It is best to ask the man himself, up on the management section of Craven's website:

"Mark Pajak's duties include chairing the investment committee and direct board level involvement with the portfolio companies. Prior to his role at Craven House Capital, Mr. Pajak was Managing Director at Desmond Holdings and a member of their investment committee. He is also President and CEO of DLC Holdings Corp. (formerly Desmond Investments Ltd), a company listed on the TSX Venture Exchange in Toronto.

Mr. Pajak started his career at Taylor Wimpey Plc, the UK's largest property developer where he worked directly for the Chief Executive advising on M&A activity, corporate capital structuring and communications with shareholders and the financial community. He was among the youngest directors in the 130 year history of the company.

Mark holds both an undergraduate degree and MBA from Oxford University."

Note the two highlighted pieces. Mr. Pajak is the CEO of DLC on the Toronto Stock Exchange and worked with a property developer, specifically advising in M&A activities. Let's check out what DLC is up to:

DLC is a shell that will have a reverse takeover to publicly list Craven, and Ceniako, one of Craven's four acquisitions listed above. KwikBuild, noted as a company related to Craven, is a South African builder of homes.

So now we know that the head of the firm that purchased more than 30% of LMFA's shares has bought private companies and then taken them public through reverse takeovers in the past. Companies with beach front properties. In our opinion at a minimum, Mr. Pajak would be purchasing LMFA shares to expand its financing business to some of his other deals.

Recall the final piece of this puzzle. The address and phone number used by Mark Pajak on the 13D filing:

107 West Federal St, PO Box 480 Middleburg VA

+1 540 687 3166

Here it is again, owned by Wallach & Company:

While small companies do often share office space, it would be unusual to see them share a PO Box number and phone number. What's more, Wallach is the only company associated with this address other than Craven when doing an internet search. Wallach doesn't seem too active, for instance, there are no Yelp or BBB reviews. But there is one news article about this insurance company and it serves 15,000 clients a year. So it is a small operation that seems to focus on health insurance to those who are travelling abroad. This is very likely the synergistic Virginia based travel insurance brokerage company that LMFA made mention of in its Q3 results.

So what does all this stuff mean?

Craven House Capital made a significant investment - both in terms of a large stake and a high proportion of its funds - into LMFA. LMFA provides financial solutions for condo associations. Craven has a history of doing reverse takeover transactions and invests in property development projects. What's more, it shares a mailing address and phone number of a company that offers health insurance to those travelling abroad and used that specific address on its 13D filing with the SEC.

What is our conclusion from all this? Craven's investment into LMFA is part of something bigger. We strongly believe that there will be a reverse takeover, just like with DLC in Canada, and it could involve one or more of Craven's other assets. Development of a resort property in Brazil might be where this is headed.

If you were caught at a bad price in the volatile trading of LFMA recently, do not fear. Craven House Capital likely has big plans for this investment. Look at what happened to YECO when it announced the close of its reverse merger deal to buy the Millennium Sapphire.

Disclosure: We are long LMFA

Bitcoin has gone from a concept worth pennies a few years ago to worth thousands of dollars. It may appear to some who are late to the game that the opportunity to get rich is gone. However, there are still plenty of ways to make some money trading in bitcoin and other cryptocurrency. Here are some links to valuable reports and strategies:

The Cryptocurrency Codex from the Cryptocurrency Institute

Secrets To Unlimited Free Bitcoin

The Crypto-Currency Evolution eBook

Bitcoin Complete Guide for Dummies

The Bitcoin Miracle Guide

The Bitcoin Cheat Code Book

The Crpytocurrency Course

Bitcoin Investing Live

If you're interested in making money investing or trading the stock market, here are some good resources to assist you. This includes technical analysis, investing in the weed sector, dividend stock investing, gold and commodities, sector rotation, options trading and microcap trading strategies.

Microcap Millionaires Free Video: Cheap Gold Miner Set to Soar in Fall 2017

The dividend stock report from dividendstocksonline.com

The dividend stock report from Dividend Stocks Rock

Top rated signals for binary options from binaryoptionsprosignals.com

Goldmasterinvesting.com Ocean Of Gold Report for the top 15 gold mining companies

Trader Review shows how to time the market with its "Percent of X" indicator

The Trader's Academy Club

The Wealth Builder's Club from beatthemarketanalyzer.com

MyBB: A Forum For Investors and Traders

Spartan Trader Forex Academy Live Daily Trading Room

Try the Z Code System if you're looking for other ways to make money systematically outside of the stock market.

Top rated signals for binary options from binaryoptionsprosignals.com

Goldmasterinvesting.com Ocean Of Gold Report for the top 15 gold mining companies

Trader Review shows how to time the market with its "Percent of X" indicator

The Trader's Academy Club

The Wealth Builder's Club from beatthemarketanalyzer.com

MyBB: A Forum For Investors and Traders

Spartan Trader Forex Academy Live Daily Trading Room

Try the Z Code System if you're looking for other ways to make money systematically outside of the stock market.

No comments:

Post a Comment